TEXT A: DEMAND AND SUPPLY

| Key terms: supply, demand, buying behaviour, microeconomics, decision-making unit, effectivedemand, consumer preferences, purchasing choice, utility, buying decision, demand relationship, supply relationship, opportunitycost, the Law of Supply, the Law of Demand, market equilibrium, elasticity, quantity demanded, quantity supplied. Other words and expressions:to make economic choices, to consume goods and services, under condition of competition, by way of operation, to determine the price of, to be equal to, to refer to, the ability and the willingness to pay, to be affected by, a significant impact, to be available for, the backbone of a market economy, the correlation between, to underlie the forces, allocation of resources, to forgo the consumption of something, to increase revenue, the long-term levels of demand, equipment and production facilities, to shape the market, to reach compromise. Linking words and phrases:let’s have a close look at; to sum up; in other words; as a result; unlike; however; so far; obviously; in most cases; thus; so; conversely; on the other hand; we would say. |

All societies necessarily make economic choices. Society needs to make choices about what should be produced, how those goods and services should be produced, and who is allowed to consume those goods and services. For conventional economics, the market answers these questions by way of the operation of supply and demand. Under conditions of competition, where no one has the power to influence or set price, the market (everyone, producers and consumers together) determines the price of a product, and the price determines what is produced, and who can afford to consume it.

The terms suppl y and demand do not mean the amount of goods and services actually sold and bought; in any sale the amount sold is equal to the amount bought, and such supply and demand, therefore, are always equal.

Let’s have a closer look at both of them.

In microeconomics, demand refers to the buying behaviour of a household. What does this mean? Basically, micro economists want to try to explain three things:

1. Why do people buy what they buy?

2. How much are they willing to pay?

3. How much do they want to buy?

Demand is comprised of three things.

· Desire

· Ability to pay

· Willingness to pay

It is not enough to merely want or desire an item. One must show the ability to pay and then the willingness to pay. If all three conditions are not met then the demand is not real.

Each household, or small-scale decision-making unit, is affected by different factors when making choices about what to buy and how much to buy. Consumer preferences weigh heavily in a household's buying decisions. Another factor that affects such decisions is income: a millionaire and an average citizen will have very different purchasing choices, since they have different budgets to work on. All buyers will try to maximize their utility, that is, make themselves as happy as possible, by spending what money they have in the best way possible. By considering both their preferences and their budget, they ensure that they end up with the best combination of goods possible. Because the household is such a small unit, no household has a significant impact on the market, and so the actions of any single household is its best effort to react to the market price and the goods available.

At the other side of every transaction is a seller. Economists refer to the behaviour of sellers as the market force of supply. It is the combined forces of supply and demand that make up a market economy. Firms operate independently of each other, making decisions about what to sell, and how much to sell, depending on the price. How do firms make their selling decisions? Once they have decided what to sell, (a decision they make is based on what they believe buyers will want to buy), their decision is then influenced by the market price of the goods.

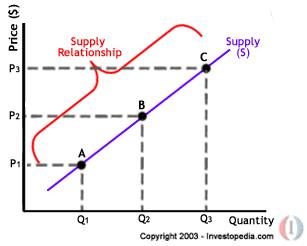

Supply and demand is perhaps one of the most fundamental concepts of economics and it is the backbone of a market economy. Demand refers to how much (quantity) of a product or service is desired by buyers. The quantity demanded is the amount of a product people are willing to buy at a certain price. The relationship between price and quantity demanded is known as the demand relationship. Supply represents how much the market can offer. The quantity supplied refers to the amount of a certain good producers are willing to supply when receiving a certain price. The correlation between price and how much of a good or service is supplied to the market is known as the supply relationship. Price, therefore, is a reflection of supply and demand.

The relationship between demand and supply underlie the forces behind the allocation of resources. In market economy theories, demand and supply theory will allocate resources in the most efficient way possible. How? Let us take a closer look at the Law of Demand and the Law of Supply.

A. The Law of Demand

The Law of Demand states that, if all other factors remain equal, the higher the price of a good, the less people will demand that good. In other words, the higher the price, the lower the quantity demanded. The amount of a good that buyers purchase at a higher price is less because as the price of a good goes up, so does the opportunity cost of buying that good. As a result, people will naturally avoid buying a product that will force them to forgo the consumption of something else they value more.

B. The Law of Supply

Like the Law of Demand, the Law of Supply demonstrates the quantities that will be sold at a certain price. But unlike the Law of demand, the supply relationship shows an upward slope. This means that the higher the price, the higher the quantity supplied. Producers supply more at a higher price because selling a higher quantity at a higher price increases revenue.

C. Equilibrium

So far, we've looked at supply, we've looked at demand, and the main question that now arises is: "How do these two opposing forces of supply and demand shape the market?" Buyers want to buy as many goods as possible, as cheaply as possible. Sellers want to sell as many goods as possible, at the highest price possible. Obviously, they can't both have their way. How can we figure out what the price will be, and how many goods will be sold? In most cases, supply and demand reach some sort of compromise on the price and quantity of goods sold: the market price is the price at which buyers are willing to buy the same number of goods that sellers are willing to sell. This point is called market equilibrium. Because supply and demand can shift and change, equilibrium in a standard market is also fluid, responding to changes in either market force.

When supply and demand are equal (i.e. when the supply function and demand function intersect) the economy is said to be at equilibrium. At this point, the allocation of goods is at its most efficient because the amount of goods being supplied is exactly the same as the amount of goods being demanded. Thus, everyone (individuals, firms, or countries) is satisfied with the current economic condition. At the given price, suppliers are selling all the goods that they have produced and consumers are getting all the goods that they are demanding.

In the real market place equilibrium can only ever be reached in theory, so the prices of goods and services are constantly changing in relation to fluctuations in demand and supply.