In a competitive global world, the measurement of the worth of the organisation lies not just in its material wealth but also in the intangible assets/intellectual capital. These are the procedures, know-how, experience and skills that propel the organisation into its highest level of proficiency and efficiency. Tacit Knowledge is normally controlled and owned by the employees in the organisation. Traditionally, an organisation responds by predicting and reacting using pre-programmed heuristics measures. Today, the organisation demands from employees to be proactive and respond to the faster cycle of knowledge-creation. The intellectual capital can consist of three different areas:

Human capital consists of skills, experiences and expertise of the people in the organisation. Human capital is embedded in the organisation as tacit, complex, not articulated and not documented. It is difficult to capture or document this knowledge in a simple and articulated format. It is important for an organisation to realise the importance of human capital and make an effort to capture and maintain this type of knowledge within the organisation. Encouraging knowledge sharing and knowledge transfer between people within the organisation is one of the methods that can be effectively employed to manage human capital. Encouraging staff to participate in seminars, workshops, continuous education is another way of enhancing the human capital within the organisation

Customer capital consists of business transactions, customer satisfaction and relations. Customer capital is relatively easier to capture as opposed to human capital. Some performance indices can be used to measure the customer capital, such as repeat business transactions, market dominance due to market strategy, customer feedback and so on. In order to capture customer capital, it is a pre-requisite to have a comprehensive database to capture the business transactions. Some IT applications such as data warehousing and data mining are used to generate these performance indices or customer capital.

Structural capital consists of manuals, databases, procedures, and company culture and practices. They are the technologies, methodologies and processes that enable an organisation to function. For example, a company may have a comprehensive information system that uses many computer-based applications such as financial system and material management system, etc. These applications are running on a computer system and information is transmitted over a network infrastructure.

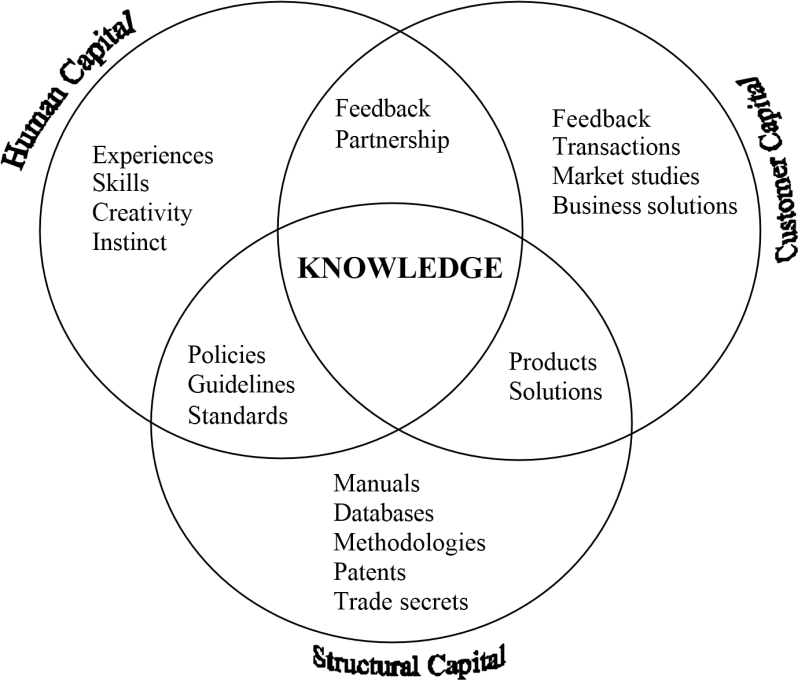

Intellectual capital unlike tangible assets does not appear in the balance sheet of the organisation. However, it is an element in the organisation that shapes the “character” of the organisation. Intellectual capital includes inventions, technologies, ideas, general knowledge, computer programs, design, data, skills, experience, processes, creativity, publications and so on. Figure 1 shows the three different areas discussed above which contribute to intellectual capital. With Knowledge at the centre of the diagram, we can see the three components of intellectual capital and the overlap between these components. The ability to recognise and capture the know -how is essential to add value to the organisation. One ways in which organisations can manage intangible assets is by aligning performance with business strategies. This model looks at both organisational and individual factors that affect performance, and focuses on obtaining measurable outcomes that benefit the individual and the organisation. Another approach is to identify core functions in the business process. This involves the study of different aspects of the business process and identifying the critical areas that are not in any physical form but crucial to the various operations in the organisation. Collaborative tools such as Intranet, workflow, interest groups, forums and interviews can facilitate pulling experiences and insights from individuals within the organisation.

Fig 2.1: Components of Intellectual capital

Sharing insights and best practices is a behaviour that is critical to the success of any knowledge management system, yet getting individuals to share their knowledge is counter to the culture found in most organisations. This is the biggest obstacle to successful knowledge management. Employees are more likely to share knowledge if it is linked with common goals of the organisation and achieves clear economic value. Knowledge sharing, is about contribution, respect for others’ opinions and views, as long as all stakeholders are able to visualise the positive influences of information and appreciate the best way to practice using information; information can be effectively and profitably transferred into knowledge.

It is also important to incorporate lessons learnt form the entire chain of events that are always happening in the organisation. This could be obtained from customer feedback, product design, delivery channels and packaging, etc. An organisation can only retain its position and be strong in the competitive global market only if it corporate this into its business workflow and strives to improve on its strength continuously.

The most direct source of valuable information to the organisation is from the customers. If the customers’ feedback is captured and the necessary lessons learnt, it can be incorporated into its current business workflow. This shows that the organisation is concerned and cares about its customers. It is also important to foster a closer employee-to-customer relationship. This will eventually grow into an everlasting bond that helps the organisation to be effective in capturing its intangible asset.

Assignments

1. What areas are included in the public intellectual capital?

2. What are the main components of corporate capital?

Fig. 2.2 Corporate Capital Components

3. Can you explain the structure of the customer capital?

4. What do you know about structural capital?

5. Explain how human, customer and structural capitals are interrelated. The figure below may be helpful.

Fig. 2.3 Human, Customer and Strucrural Capital Interrelation

6. What kind of capital does not appear in the balance sheet? Why?

7. What collaborative tools do you know and what is their role?

8. How is it possible to use customer’s feedback in the organization?

9. How does intellectual capital work?

10. Summarize the text.

Text 3